Just ten years ago the international community came together to react to the global economic and financial crisis. In the aftermath of 2008, the concerted actions of the G20 members to stimulate their economies and refrain from protectionist measures were crucial to avoid another Great Depression (Summers and Schoenfeld 2012). The global economy returned to positive growth again by 2010. But that consensus did not last. Since 2010 governments started to differ in their readings of the origins of the crisis, the challenges ahead, and the policies to adopt, which in turn led to a suboptimal global policy mix. Global growth was slow in picking up afterwards, and while it accelerated in 2017, it is now under the threat of increased downside risks (IMF 2018).

Clouds are gathering on the outlook 2017 marked a positive turning point for the global economy, with global output expanding by 3.9%. Growth has been broad-based and synchronised across the world. The EU economy grew at its fastest rate in ten years at 2.4%, US and Japan also grew strongly. Emerging economies did well: China and India grew by 6.9% and 6.4%, respectively. In the latest European Commission Summer Forecast published on 11 July (European Commission 2018b), we project a further acceleration in global growth to 4.2% in 2018 and 4.1% in 2019. While the headline figures are still positive, much has changed recently. The US policy mix has become pro-cyclical due to a significant fiscal expansion. Trade tensions are escalating on the back of China's over-capacity, which prompted the US decision to impose import tariffs on steel and aluminium. These developments have added to the already existing uncertainties related to geopolitical risks and have greatly increased the possibility of a slowdown in global growth.

Such developments build on growing institutional, economic and social fragmentation across the world which set in during the financial crisis.

Institutional fragmentation has increased In the wake of the crisis, the G20 emerged as the premier forum for international economic and financial cooperation around the world. In parallel, a host of new institutions have been created often with overlapping mandates and no clear roadmap for cooperation. For example, new multilateral development banks (MDBs) were created in Asia (the Asia Infrastructure Investment Bank) and by the BRICS countries (New Development Bank) and regional financing arrangements became more prominent in providing emergency liquidity alongside the IMF; this has increased the financial firepower but also the complexity of the system. The WTO effectiveness has been weakened by the adoption of unilateral trade measures in some countries and by the failure to agree on new nominations for the Appellate Body. Global efforts to tackle climate change have been compromised by the US decision to abandon the UN Paris Agreement on Climate Change. Tensions among world leaders were manifest also at the last G7 Summit in Canada in June 2018. There is now the risk that the G20 might fail to ‘win the peace’, i.e. to deliver the necessary public good of global economic policy cooperation in the post-crisis world. (Buti and Bohn-Jespersen 2016).

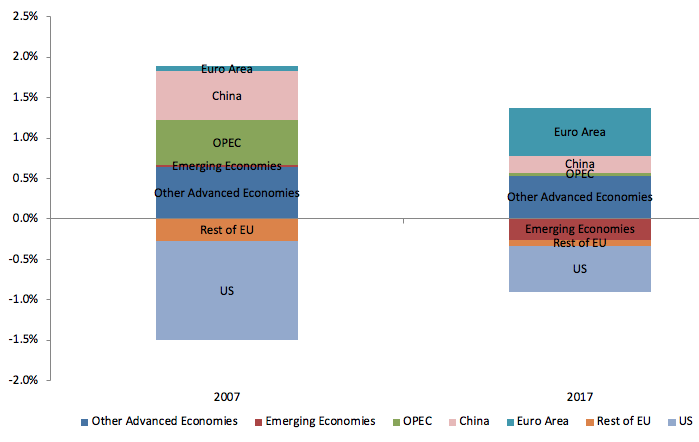

Economic and social fragmentations remain pervasive Since the outbreak of the crisis, global imbalances have been reduced but they remain considerable. Two developments stand out. First of all, emerging countries now have, on aggregate, current account deficits (Figure 1). Large current account surpluses can now be found among advanced economies. The US records a persistent current account deficit which may now further increase due to pro-cyclical fiscal policies. Second, the single largest source of external surpluses is now the euro area. This is due in part to an asymmetric rebalancing within the monetary union, where countries that used to have current account deficits prior to the crisis have turned them into surpluses but pre-crisis surplus countries have remained in surplus and sometimes increased it. These developments imply potential fragilities for emerging economies and rising trade tensions among advanced countries.

Figure 1 Global imbalances: Current accounts as a percentage of world GDP

Source: Own calculations based on IMF WEO Database and World Bank Database

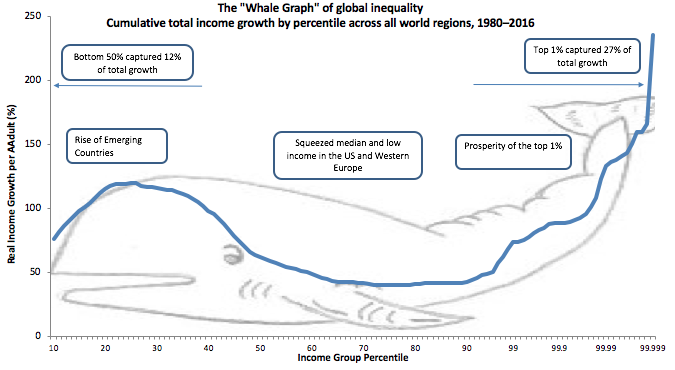

Social fragmentation has started to receive more attention recently (Figure 2). While inequality between emerging and advanced countries has been reduced, inequalities within countries have surged since the 1980s. The increase in income inequality at global level hides important differences across countries. In emerging economies inequalities are higher but they have slowly been reduced over the past 30 years. Conversely, advanced countries such as the old member states of the EU and the US have seen income inequality increasing. Globalisation and trade integration have contributed to the increase in income inequality through skill-based and geographical distributional impacts. Nation states and multilateral institutions failed to adequately counter these trends so far. Socioeconomic and regional inequalities fuel popular discontent and opposition to economic openness and international cooperation, leading governments to revert to inward-looking policies and protectionism.

Figure 2 Social fragmentation

Source: Own calculations based on World Inequality Database

雷达卡

雷达卡

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 变色卡

变色卡 抢沙发

抢沙发 千斤顶

千斤顶 显身卡

显身卡

京公网安备 11010802022788号

京公网安备 11010802022788号