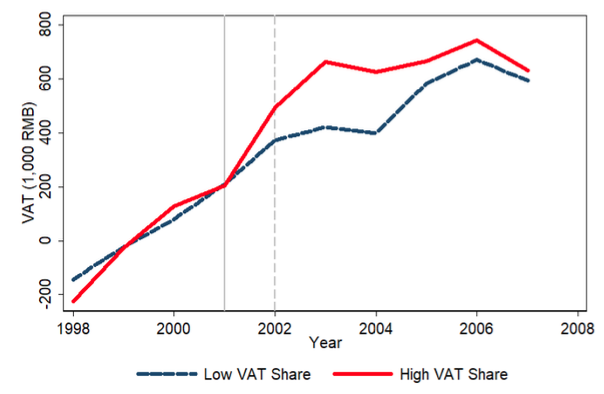

Figure 1 Mean VAT

Notes: The data are normalised to be visually comparable. The pre-computerisation mean of each group is subtracted from the value of each year in the group.

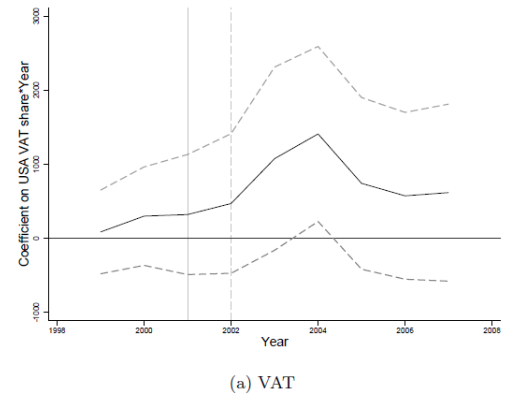

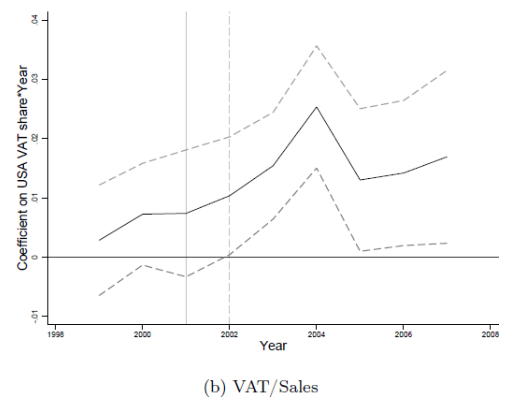

This general pattern remains when we control for more variables. In Figure 2, we present the estimated difference between high VAT share firms and low VAT share firms. By controlling for year fixed effects and firm fixed effects, we remove any variation that affected all firms equally in a given year, as well as any long-run differences between firms. We also control for initial size interacted with year fixed effects, which absorb any differences in firm behaviour by size within each year. Just as in Figure 1, we observe that VAT payments increase differentially for high VAT share firms until 2004, at which point they begin to decline.

Figure 2 Estimates for VAR and VAT/sales

Notes: These figures plot the interaction coefficients of VAT Share and year dummy variables (controlling for the interaction of pre-computerization average sales and year fixed effects, and year and firm fixed effects) and their 90% confidence intervals. The sample is a balanced panel of firms, 1998-2007. The reference year is 1998.

We explain these results with a simple framework. Suppose that firms can respond to policy changes, but some of their inputs, like fixed capital, cannot be adjusted quickly. In such a scenario, an increase in tax enforcement will increase effective tax rates. Firms will wish to downsize in response to the increase in effective tax rates, but they cannot change all their inputs. In the short run, limited firm downsizing and the increase in tax rates will lead to an increase in overall tax revenues (if demand is not too elastic). However, in the long run, firms will be able to fully adjust in response to the new tax regime. They will choose fewer inputs and produce less output, and this effect will attenuate the increase in tax revenue.

This explanation has implications for other firm observables as well; it suggests that over time, firm sales, inputs, and employment should decrease steadily. Moreover, productivity, which is conceptually similar to the ratio of output to total inputs, should increase steadily. When we examine these variables, we find that they behave consistently with our interpretation. The increase in VAT causes firms to contract in the medium run.

An alternative interpretation for the short-run increase and the long-run attenuation in VAT payments is that firms learned to evade again over time. Anecdotal evidence suggests that evasion still exists – firms may purchase legitimate invoices from a black market. This explanation implies that the deductible inputs of firms, after a short-term decline, should rise again as firms learn how to falsify deductibles under the new system. However, when we examine deductible inputs, we find that they decline monotonically over time. Thus, there is little evidence that firms learn new ways of evasion.

These patterns suggest that information technology can improve state capacity in a developing country context. This result relates to a literature exploring the role of technology in governance. For example, Duflo et al. (2012) provide experimental evidence that time-stamped photographs improve teacher attendance in India, and Muralidharan et al. (2016) show that biometric technology improves the delivery of state subsidies in rural India.

We also enlarge the body of evidence on firm responses to tax enforcement (Kumler et al. 2013, Naritomi 2015, Pomeranz 2015, Carrillo et al. 2017). Our estimates provide novel empirical evidence that medium- or long-run effects are likely to differ from short-run effects. In particular, we argue that firms may downsize in response to an increase in tax enforcement, and that these real effects can decrease the gains in tax revenue due to better enforcement, especially in the long run.

ReferencesCarrillo, P, D Pomeranz, and M Singhal (2017), “Dodging the Taxman: Firm Misreporting and Limits to Tax Enforcement,” American Economic Journal: Applied Economics 9(2): 144–64.

Duflo, E, R Hanna, and S P Ryan (2012), “Incentives Work: Getting Teachers to Come to School,” American Economic Review 102(4): 1241–1278.

Gordon, R H and W Li (2009), “Tax Structures in Developing Countries: Many Puzzles and a Possible Explanation,” Journal of Public Economics 93(7-8): 855–866.

Keen, M and B Lockwood (2010), “The Value-Added Tax: Its Causes and Consequences,” Journal of Development Economics 92(2): 138–151.

Kleven, H J, M B Knudsen, C T Kreiner, S Pedersen, and E Saez (2011), “Unwilling or Unable to Cheat? Evidence From a Tax Audit Experiment in Denmark,” Econometrica 79(3): 651–692.

Kumler, T, E Verhoogen, and J A Frias (2013), “Enlisting Employees in Improving Payroll-Tax Compliance: Evidence from Mexico,” NBER Working Paper 19385.

Muralidharan, K, P Niehaus, and S Sukhtankar (2016), “Building State Capacity: Evidence from Biometric Smartcards in India,” American Economic Review 106(10): 2895–2929.

Naritomi, J (2015), “Consumers as Tax Auditors,” Working paper, London School of Economics.

Pomeranz, D (2015), “No taxation without information: Deterrence and self-enforcement in the value added tax,” American Economic Review 105(8): 2539– 2569.

雷达卡

雷达卡

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 变色卡

变色卡 抢沙发

抢沙发 千斤顶

千斤顶 显身卡

显身卡

京公网安备 11010802022788号

京公网安备 11010802022788号