69 个论坛币

69 个论坛币

雷达卡

雷达卡

随着人工智能技术的飞速发展,它正在重塑财务金融研究的面貌。

如何跨越传统边界,并了解AI如何赋能财务金融研究及论文发表?

来12月4日计量与统计直播间,

南京农业大学金融学院会计系主任,财政部高层次财会人才汤晓建教授将在本次直播中分享他的独到见解和研究成果:

直播亮点:

→ AI在财务金融研究中的应用与前景

→ 如何利用AI技术提升研究效率和论文质量

→ 汤教授的研究成果和论文发表经验分享

→ 互动环节:与专家直接对话,解答您的疑问

深入探讨AI在财务金融领域的应用,并

通过实战案例操作掌握论文写作发表的秘籍:

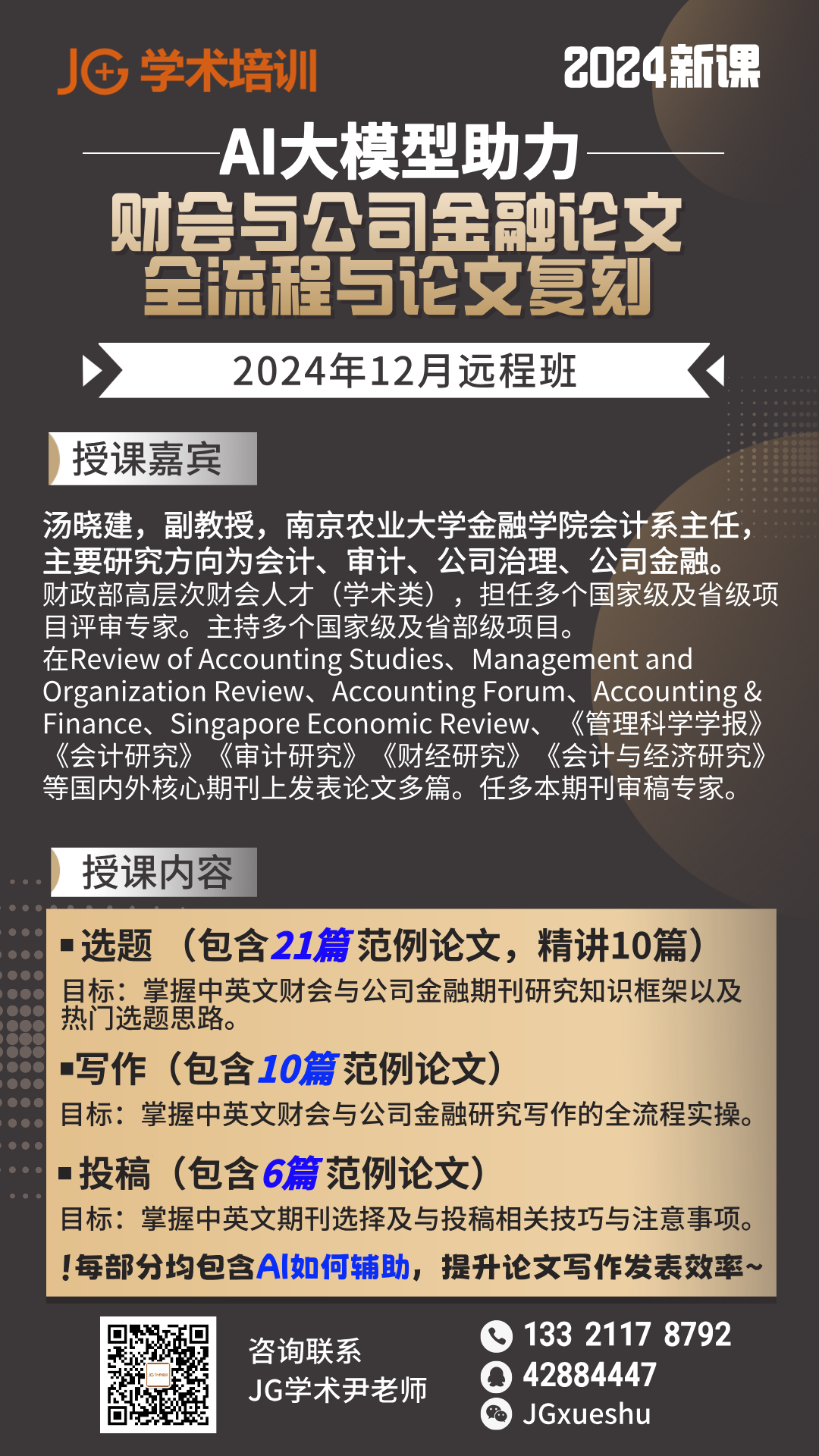

Al大模型助力财会与公司金融论文全流程与论文复刻

每部分均包含AI如何辅助,提升论文写作发表效率~

培训时间:2024年12月14-15, 21日 (周末三天)

授课安排:9:00-12:00;14:00-17:00;答疑交流

培训地点:远程直播,提供录播回放

讲师介绍:

汤晓建,南京农业大学金融 学院会计系主任,副教授,中山大学会计学博士,东北财经大学会计学博士后,中国会计学会会计教育分会理事。主要研究方向为会计、审计、公司治理、公司金融。

入选2022年度财政部高层次财会人才素质提升工程(中青年人才培养-学术班),担任江苏省科技厅、山东省科技厅、南京市科技局项目评审专家,CSMAR新库评审专家,国家自然科学基金通讯评审专家等。

主持国家自然科学基金青年项目1项,教育部人文社科项目2项、中国博士后科学基金特别资助1项,中国博士后科学基金面上项目(一等资助)1项,江苏省教育厅高校哲学社会科学研究项目1项,江苏省社科应用研究精品工程财经发展专项3项,中央高校基本科研业务费项目4项,参与研究阐释党的十九大精神国家社科基金专项、国家自然科学基金重点项目、国家自然科学基金重大项目等国家、省部级项目5项。

在Review of Accounting Studies、Management and Organization Review、AccountingForum、Accounting& Finance、SingaporeEconomic Review、《管理科学学报》《会计研究》《审计研究》《财经研究》《会计与经济研究》《证券市场导报》《上海财经大学学报》等国内外核心期刊上发表论文多篇。曾获2020年度江苏省社科应用研究精品工程(财经发展专项)奖一等奖,首届“审计与国家治理现代化”研讨会最佳论文奖,2022年度江苏省社科应用研究精品工程(财经发展专项)奖三等奖。

课程特色:

1. 顶级期刊选题与写作思路解读:深入剖析JAR等顶级期刊的选题与写作技巧。

2. 论文复刻实操:通过论文精讲,分享如何复刻论文,包括数据 分析全过程。

3. Stata范例教学:研究方法中Stata范例会分享do文档与对应范例,无需Stata基础。

4. 实战案例分析:结合中文及英文论文复刻,深入讲授财会与公司金融实证论文中的前沿研究、选题思路与方法设计。

适用人群:

1. 会计学:对于会计学专业的学生来说,这门课程将帮助他们深入理解会计研究的前沿动态,提升论文写作和研究能力。

2. 审计学:审计专业的学生可以通过课程学习如何运用AI技术进行更有效的审计研究和论文撰写。

3. 财务管理:财务管理专业的学生将从课程中获得有关公司金融领域的最新研究成果和研究方法。

4. 公司治理:公司治理专业的学生可以学习如何通过AI技术优化公司治理结构和提高治理效率。

5. 公司金融:公司金融专业的学生将学习到如何进行高质量的金融研究,以及如何将研究成果发表在顶级期刊上。

6. 经济学:经济学专业的学生可以通过课程了解如何将经济学理论应用于财会和公司金融的实际问题研究中。

7. 管理 学:管理学专业的学生可以学习如何运用AI技术提高管理决策的科学性和有效性。

8. 数据科学与大数据技术:对于数据科学和大数据技术专业的学生,这门课程提供了一个将数据分析技能应用于财会和金融领域的实践机会。

9. 金融工程:金融工程专业的学生可以通过课程学习如何运用AI和大数据技术进行金融产品的设计和风险管理。

10. 国际商务:国际商务专业的学生可以学习如何在国际背景下进行财会和金融研究,以及如何将研究成果发表在国际期刊上。

课程大纲:

第1讲:财会与公司金融论文选题(PPT+ do文件+dta数据)

目标:掌握中英文财会与公司金融期刊研究知识框架以及热门选题思路。

内容:

论文选题的基本逻辑;

研究想法的寻找与选择;

理论研究情境化(信息披露、公司税收、人工智能、气候金融和ESG等研究主题);

研究设计与方法讨论(内生性问题处理,应用Stata进行中文及英文论文复刻等);

AI如何辅助选题。

范例论文(精讲10篇):

[1] Cao, S., Jiang, W., Yang, B., & Zhang, A. L.(2023).How to talk when a machine is listening: Corporate disclosure in the ageof AI. The Review of Financial Studies, 36(9), 3603-3642.

[2] Chen,T., Harford, J., & Lin,C. (2015). Do analysts matter for governance? Evidence from naturalexperiments. Journal of financial Economics, 115(2),383-410.

[3] Chen,Y. C., Hung, M., & Wang,Y. (2018). The effect of mandatory CSR disclosure on firm profitability andsocial externalities: Evidence from China. Journal of Accounting and Economics,65(1), 169-190.

[4] Christensen,D. M., Serafeim, G.,& Sikochi, A. (2022). Why is corporate virtue in the eye of the beholder?The case of ESG ratings. The Accounting Review, 97(1),147-175.

[5] Flammer, C. (2021). Corporate green bonds. Journal offinancial economics, 142(2), 499-516.

[6] Krueger, P., Sautner, Z., & Starks, L. T. (2020).The importance of climate risks for institutional investors. The Review offinancial studies, 33(3), 1067-1111.

[7] LaPorta, R., Lopez-de-Silanes, F.,&Shleifer, A. (2006). What works in securities laws?. The journal offinance,61(1), 1-32.

[8] Leippold, M., Wang, Q., & Zhou, W. (2022).Machine learning in the Chinese stock market. Journal of Financial Economics,145(2),64-82.

[9] Lennox, C., & Wu, J. S. (2022). A review ofChina-related accounting research in the past 25 years. Journal of Accountingand Economics, 101539.

[10]Li, K., Mai, F., Shen, R., & Yan,X. (2021).Measuring corporate culture using machine learning. The Review of FinancialStudies, 34(7), 3265-3315.

[11]Lu, H., Shin, J. E., & Zhang, M.(2023). Financialreporting and disclosure practices in China. Journal of Accounting andEconomics, 101598.

[12] Raghunandan, A., & Rajgopal,S. (2022). Do ESG funds make stakeholder-friendly investments?. Review ofAccounting Studies, 27(3), 822-863.

[13]Shen, H., Lin, H., Han, W., & Wu,H. (2023). ESG inChina: A review of practice and research, and future research avenues. ChinaJournal of Accounting Research, 100325.

[14]Starks, L. T. (2023). Presidential address:Sustainable finance and ESG issues—value versus values. The Journal of Finance,78(4), 1837-1872.

[15] Stigler, G. J. (1963).Publicregulation of the securities markets. Bus. Law., 19, 721.

[16]Stroebel, J., & Wurgler, J. (2021).What do youthink about climate finance?. Journal of Financial Economics,142(2), 487-498.

[17] Yost, B. P., & Shu,S. (2022).Does tax enforcement deter managers' self-dealing?. Journal of Accounting andEconomics, 74(1), 101512.

[18] 李增福,骆展聪,杜玲等.“信息机制”还是“成本机制”?——大数据税收征管何以提高了企业盈余质量[J].会计研究,2021(07):56-68.

[19] 刘慧龙,张玲玲,谢婧.税收征管数字化升级与企业关联交易治理[J].管理世界,2022,38(06):158-176.

[20] 魏志华,王孝华,蔡伟毅.税收征管数字化与企业内部薪酬差距[J].中国工业经济,2022,No.408(03):152-170.

[21] 张克中,欧阳洁,李文健.缘何“减税难降负”:信息技术、征税能力与企业逃税[J].经济研究,2020,55(03):116-132.

第2讲:财会与公司金融论文写作(PPT+ do文件+dta数据)

目标:掌握中英文财会与公司金融研究写作的全流程实操。

内容:

论文写作的基本逻辑;

写作思路与注意事项;

经典论文写作剖析;

AI如何辅助写作。

范例论文(10篇):

[1] Cheng,Q., Hail, L., & Yu, G.(2022). The past, present, and future of China-related accounting research.Journal of Accounting and Economics,74(2-3), 101544.

[2] Ke,B., Lennox, C. S., & Xin,Q. (2015). The effect of China's weak institutional environment on the qualityof Big 4 audits. The Accounting Review, 90(4),1591-1619.

[3] Lennox,C., & Wu, J. S. (2022).A review of China-related accounting research in the past 25 years. Journal ofAccounting and Economics, 74(2-3), 101539.

[4] Pan,Y., Shroff, N., & Zhang,P. (2023). The dark side of audit market competition. Journal of Accounting andEconomics, 75(1), 101520.

[5] Xu,N., Li, X., Yuan, Q., &Chan, K. C. (2014). Excess perks and stock price crash risk: Evidence fromChina. Journal of Corporate Finance, 25, 419-434.

[6] 蔡贵龙,柳建华,马新啸.非国有股东治理与国企高管薪酬激励[J].管理世界,2018,34(05):137-149.

[7] 冯晨,周小昶,田彬彬,等.税收稽查体制改革与企业集团资本结构调整 [J]. 经济研究,2023, 58 (08): 100-119.

[8] 潘健平,翁若宇,潘越.企业履行社会责任的共赢效应——基于精准扶贫的视角[J].金融研究,2021(07):134-153.

[9] 权小锋,贺超,醋卫华,等.品牌的力量:名牌产品与盈余管理 [J]. 会计研究,2022, (01): 44-58.

[10] 权小锋,李闯.智能制造与成本粘性——来自中国智能制造示范项目的准自然实验 [J]. 经济研究,2022, 57 (04): 68-84.

第3讲:财会与公司金融论文投稿

目标:掌握中英文期刊选择及与投稿相关技巧与注意事项。

内容:

中英文期刊识别与选择;

投稿人视角解读;

审稿人视角解读;

AI如何辅助投稿。

范例论文(6篇):

[1] Du,D., Tang, X., Wang, H., Zhang,J. H., Tsui, S., & Lin, D. (2022). CEO organizational identification andcorporate innovation investment. Accounting& Finance, 62(3), 4185-4217.

[2] Tang,X., Du, D., Chen, Y., &Tsui, S. (2024). Tax authority governance and corporate internal controlquality. Accounting & Finance, 1-28.

[3] Xu,Y., Shi, W., Qin, X., Zhang,J., & Tang, X. (2022). Is identification all the same? The differentialeffects of CEO and CFO organizational identification on corporate philanthropy.Management and Organization Review, 18(1), 73-107.

[4] Zhang,J., Huo, Z., Zeng, Y., Tang,X., & Rui, O. M. (2021). Corporate value added tax avoidance. AccountingForum , 45(4), 338-362.

[5] 汤晓建,杜东英,谢丽娜,林斌.税收征管规范化改善了企业财务报告质量吗——基于税务行政处罚裁量基准的准自然实验[J].会计研究,2023(02):3-11.

[6] 张俊生,汤晓建,李广众.预防性监管能够抑制股价崩盘风险吗?——基于交易所年报问询函的研究[J].管理科学学报,2018,21(10):112-126.

课程咨询:

尹老师

电话:13321178792

QQ:42884447

WeChat:JGxueshu

京公网安备 11010802022788号

京公网安备 11010802022788号