雷达卡

雷达卡

功课上需要到。。。。

谢谢哦~~~

麻烦请教教如何用 R (或 eview 3.1 )来看是什么 arima

谢谢^^

附上一个附件。。。。

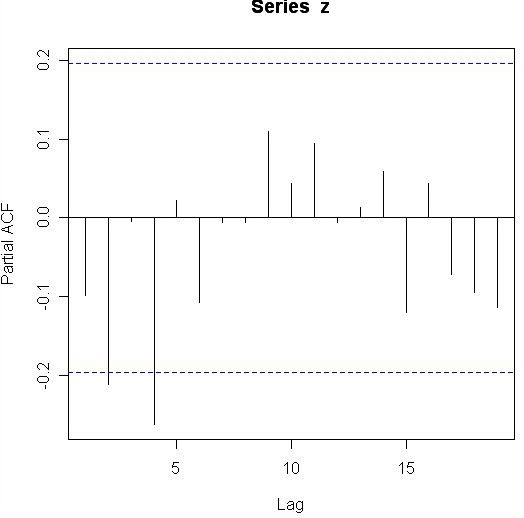

原版的 acf & pacf

经过了 First Difference 后的 acf & pacf

可是却不会看是 ARIMA (p,d,q)

能教教我吗??

谢谢 ^^

或者请教我用 eview 3.1 来看也可以。。。谢谢。。。

[此贴子已经被作者于2009-3-25 1:16:29编辑过]

|

楼主: zihau87

|

5714

10

[求助]请教一下如何用R来看是什么ARIMA...紧急!!谢谢 |

|

小学生 7%

-

|

本帖被以下文库推荐

| ||

|

|

|

|

| |||||||||

|

R is the second language for me!Using R is standing on the shoulders of giants! Let\'s use R together!

|

||||||||||

|

|

| |

|

|

| |||||||||

|

R is the second language for me!Using R is standing on the shoulders of giants! Let\'s use R together!

|

||||||||||

|

|

| |

|

|

回复:(ruiqwy)Box.test(z,lag=24)Box.test(z,lag=2...

| |

|

|

| |

|

|

| |

|

|

| |||

|

R is the second language for me!Using R is standing on the shoulders of giants! Let\'s use R together!

|

||||

|

|

| |

加好友,备注cda

加好友,备注cda京ICP备16021002号-2 京B2-20170662号

京公网安备 11010802022788号

论坛法律顾问:王进律师

知识产权保护声明

免责及隐私声明

京公网安备 11010802022788号

论坛法律顾问:王进律师

知识产权保护声明

免责及隐私声明