A benchmark modelWe also develop a benchmark small open economy model of international trade and macroeconomic dynamics that allows us to investigate what determines the dynamic effects of protectionism. The model combines key ingredients from the international business cycle literature (endogenous physical capital accumulation and nominal rigidities) with a full endogenous trade structure similar to Melitz (2003) and Ghironi and Melitz (2005).

Consistent with the focus on small economies in our empirical analysis, we assume that one of the two countries in the model is a small open economy with no impact on the rest of the world. We calibrate the model and study the consequences of a temporary increase in protectionism by the small open economy.

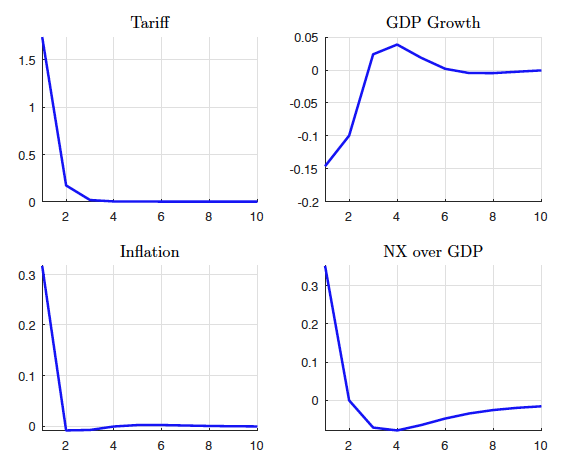

First, we focus on a tariff increase under a flexible exchange rate. This mirrors the empirical analysis described above. The predictions of the model match the robust results of the empirical evidence both qualitatively and quantitatively. Protectionism can generate a small improvement in the trade balance, but at the cost of inflation and recession (Figure 3).

Figure 3 Model-implied, annualised impulse responses to a tariff increase

Source: Barattieri et al. (2018).

Note: The tariff shock matches size and persistence of the equivalent shock in the panel VAR shown in Figure 2. Tariffs, GDP growth, and net exports over GDP are in percentage points.

The model highlights the importance of both macro and micro forces for the inflationary and contractionary effects of tariffs. Higher import prices drive CPI inflation up, and induce expenditure-switching toward domestic tradable goods. Higher tariffs also reallocate domestic market share toward less-efficient domestic producers, lowering aggregate productivity. In turn, higher domestic prices reduce aggregate real income (expenditure reduction), lowering investment in physical capital and producer entry.

Intuitively, since physical capital includes both domestic and imported goods, the import tariff increases the price of investment. Since households spend more of their real income to consume any given amount of imports, the demand for domestic goods declines, reducing the number of producers on the market.

Finally, since the trade shock acts as a supply shock, the central bank faces a trade-off between stabilising output and controlling inflation. When the response to inflation is sufficiently aggressive, the policy rate increases, further depressing current demand. Lower aggregate demand and monetary policy contraction dominate expenditure switching, causing a recession in the aftermath of an increase in protectionism. The trade balance improves, as imports decline more than exports.

Having established that our model successfully replicates the evidence, we then use it to study counterfactual scenarios for which, according to some, the use of temporary trade barriers is potentially beneficial: the presence of a zero lower bound on nominal interest rates (Eichengreen 2016) and the case of a fixed exchange rate (the recent experience of Ecuador, a dollarised economy, illustrates this scenario). Both our empirical evidence and theoretical analysis suggest that protectionism is inflationary. Through this channel, protectionism may help lift economies out of liquidity traps by reducing the real interest rate. In the second counterfactual, in which monetary policy is constrained by an exchange rate peg, the absence of exchange rate appreciation could strengthen the expenditure switching effect of tariffs.

Protectionism is costlyContrary to basic, partial-equilibrium intuitions, we find that protectionism is contractionary in both counterfactuals. The negative effects of higher tariffs on aggregate investment, and the reallocation toward less efficient producers, continue to dominate other effects. This conclusion is robust under a variety of alternative scenarios.

In sum, protectionism is costly – at least for small open economies – even when it is used temporarily, even when economies are stuck in liquidity traps, and regardless of the flexibility of the exchange rate. The detrimental economic effects arise even abstracting from retaliation from trade partners.

ReferencesBarattieri, A, M Cacciatore, and F Ghironi (2018), "Protectionism and the Business Cycle", CEPR Discussion Paper 12693.

Bown, C P (2016), Global Antidumping Database, The World Bank.

Bown, C P and M A Crowley (2013), “Import Protection, Business Cycles, and Exchange Rates: Evidence from the Great Recession”, Journal of International Economics 90: 50-64.

Eichengreen, B (1981), “A Dynamic Model of Tariffs, Output and Employment under Flexible Exchange Rates”, Journal of International Economics 11: 341-359.

Eichengreen, B (1983), “Effective Protection and Exchange-Rate Determination", Journal of International Money and Finance 2: 1-15.

Eichengreen, B (2016), “What's the Problem with Protectionism?” Project Syndicate, 13 July.

Ghironi, F and M J Melitz (2005), “International Trade and Macroeconomic Dynamics with Heterogeneous Firms", The Quarterly Journal of Economics 120: 865-915.

Goldberg, P and N Pavcnik (2016), “The Effects of Trade Policy", prepared for the Handbook of Commercial Policy, edited by K Bagwell and R Staiger (2016).

Krugman, P (1982), “The Macroeconomics of Protection with a Floating Exchange Rate", Carnegie-Rochester Conference Series on Public Policy 16: 141-182.

Melitz, M J (2003), “The Impact of Trade on Intra-Industry Reallocations and Aggregate Industry Productivity", Econometrica 71: 1695-1725.

Mundell, R (1961), “Flexible Exchange Rates and Employment Policy", Canadian Journal of Economics and Political Science 27: 509-517.

Endnotes[1] HS-6 stands for Harmonised System Six-Digit. It is the most detailed level of standard disaggregation in the code system used by the World Customs Organisation to define products.

雷达卡

雷达卡

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 变色卡

变色卡 抢沙发

抢沙发 千斤顶

千斤顶 显身卡

显身卡

京公网安备 11010802022788号

京公网安备 11010802022788号