雷达卡

雷达卡

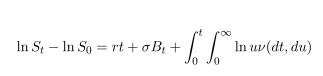

8. Assuming the stock price is driven by a mixed Poisson-Brownian motion with stock return

to be given by

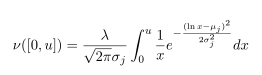

with Levy measure to be given by

Let r = 8%,σ = 12%,μ j = 0,σ j = 10%,λ = 1,S 0 = 100.

(a) Generate a sample path for the stock price process S t on [0,3].

(b) Compute E[S t ], V ar(S t ) and the m.g.f. for S t .

(c) Compute E[(100 − S T ) + ],T = 3. (Using Monte Carlo simulation, and write down

the computer code)

(d) What is the probability for the stock price to exceed 105 at time 3? (Using Monte

Carlo simulation, and write down the computer code)

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 变色卡

变色卡 抢沙发

抢沙发 千斤顶

千斤顶 显身卡

显身卡

京公网安备 11010802022788号

京公网安备 11010802022788号