关于本站

人大经济论坛-经管之家:分享大学、考研、论文、会计、留学、数据、经济学、金融学、管理学、统计学、博弈论、统计年鉴、行业分析包括等相关资源。

经管之家是国内活跃的在线教育咨询平台!

经管之家新媒体交易平台

提供"微信号、微博、抖音、快手、头条、小红书、百家号、企鹅号、UC号、一点资讯"等虚拟账号交易,真正实现买卖双方的共赢。【请点击这里访问】

期刊

- 期刊库 | 马上cssci就要更新 ...

- 期刊库 | 【独家发布】《财 ...

- 期刊库 | 【独家发布】“我 ...

- 期刊库 | 【独家发布】“我 ...

- 期刊库 | 【独家发布】国家 ...

- 期刊库 | 请问Management S ...

- 期刊库 | 英文期刊库

- 核心期刊 | 歧路彷徨:核心期 ...

TOP热门关键词

免费学术公开课,扫码加入 |

A Dark Age of macroeconomics (wonkish)

Brad DeLong is upset about the stuff coming out of Chicago these days — and understandably so. First Eugene Fama, now John Cochrane, have made the claim that debt-financed government spending necessarily crowds out an equal amount of private spending, even if the economy is depressed — and they claim this not as an empirical result, not as the prediction of some model, but as the ineluctable implication of an accounting identity.

There has been a tendency, on the part of other economists, to try to provide cover — to claim that Fama and Cochrane said something more sophisticated than they did. But if you read the original essays, there’s no ambiguity — it’s pure Say’s Law, pure “Treasury view”, in each case. Here’s Fama:

The problem is simple: bailouts and stimulus plans are funded by issuing more government debt. (The money must come from somewhere!) The added debt absorbs savings that would otherwise go to private investment. In the end, despite the existence of idle resources, bailouts and stimulus plans do not add to current resources in use. They just move resources from one use to another.

And here’s Cochrane:

First, if money is not going to be printed, it has to come from somewhere. If the government borrows a dollar from you, that is a dollar that you do not spend, or that you do not lend to a company to spend on new investment. Every dollar of increased government spending must correspond to one less dollar of private spending. Jobs created by stimulus spending are offset by jobs lost from the decline in private spending. We can build roads instead of factories, but fiscal stimulus can’t help us to build more of both.1 This is just accounting, and does not need a complex argument about “crowding out.”

Second, investment is “spending” every bit as much as consumption. Fiscal stimulus advocates want money spent on consumption, not saved. They evaluate past stimulus programs by whether people who got stimulus money spent it on consumption goods rather save it. But the economy overall does not care if you buy a car, or if you lend money to a company that buys a forklift.

There’s no ambiguity in either case: both Fama and Cochrane are asserting that desired savings are automatically converted into investment spending, and that any government borrowing must come at the expense of investment — period.

What’s so mind-boggling about this is that it commits one of the most basic fallacies in economics — interpreting an accounting identity as a behavioral relationship. Yes, savings have to equal investment, but that’s not something that mystically takes place, it’s because any discrepancy between desired savings and desired investment causes something to happen that brings the two in line.

It’s like the fact that the capital account and the current account of the balance of payment have to sum to zero: that’s true, but it does not mean that an increase in capital inflows magically translates into a trade deficit, without anything else changing (what John Williamson used to call the doctrine of immaculate transfer). A capital inflow produces a trade deficit by causing the exchange rate to appreciate, the price level to rise, or some other change in the real economy that affects trade flows.

Similarly, after a change in desired savings or investment something happens to make the accounting identity hold. And if interest rates are fixed, what happens is that GDP changes to make S and I equal.

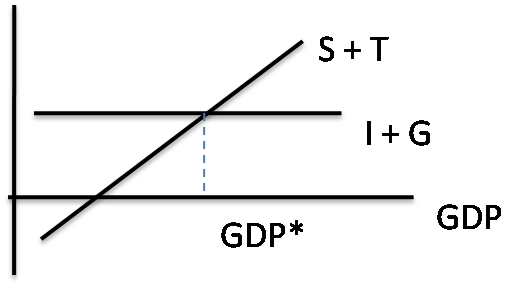

That’s actually the point of one of the ways multiplier analysis is often presented to freshmen. Here’s the diagram:

A case of mistaken identity

A case of mistaken identityIn this picture savings plus taxes equal investment plus government spending, the accounting identity that both Fama and Cochrane think vitiates fiscal policy — but it doesn’t. An increase in G doesn’t reduce I one for one, it increases GDP, which leads to higher S and T.

Now, you don’t have to accept this model as a picture of how the world works. But you do have to accept that it shows the fallacy of arguing that the savings-investment identity proves anything about the effectiveness of fiscal policy.

So how is it possible that distinguished professors believe otherwise?

The answer, I think, is that we’re living in a Dark Age of macroeconomics. Remember, what defined the Dark Ages wasn’t the fact that they were primitive — the Bronze Age was primitive, too. What made the Dark Ages dark was the fact that so much knowledge had been lost, that so much known to the Greeks and Romans had been forgotten by the barbarian kingdoms that followed.

And that’s what seems to have happened to macroeconomics in much of the economics profession. The knowledge that S=I doesn’t imply the Treasury view — the general understanding that macroeconomics is more than supply and demand plus the quantity equation — somehow got lost in much of the profession. I’m tempted to go on and say something about being overrun by barbarians in the grip of an obscurantist faith, but I guess I won’t. Oh wait, I guess I just did.

免流量费下载资料----在经管之家app可以下载论坛上的所有资源,并且不额外收取下载高峰期的论坛币。

涵盖所有经管领域的优秀内容----覆盖经济、管理、金融投资、计量统计、数据分析、国贸、财会等专业的学习宝库,各类资料应有尽有。

来自五湖四海的经管达人----已经有上千万的经管人来到这里,你可以找到任何学科方向、有共同话题的朋友。

经管之家(原人大经济论坛),跨越高校的围墙,带你走进经管知识的新世界。

扫描下方二维码下载并注册APP

您可能感兴趣的文章

本站推荐的文章

人气文章

本文标题:A Dark Age of macroeconomics (Paul Krugman)

本文链接网址:https://bbs.pinggu.org/jg/kaoyankaobo_kaoyan_423292_1.html

2.转载的文章仅代表原创作者观点,与本站无关。其原创性以及文中陈述文字和内容未经本站证实,本站对该文以及其中全部或者部分内容、文字的真实性、完整性、及时性,不作出任何保证或承若;

3.如本站转载稿涉及版权等问题,请作者及时联系本站,我们会及时处理。